Author: Ankit Baid, Research Analyst at Affluence Advisory

A Rough Start to September: Stock Market Woes and Global Economic Concerns

The first week of September was anything but favorable for stock market enthusiasts. Far from setting any positive records, the market’s performance left financiers and investors alike disheartened. As concerns over global growth intensify, the financial world turns its attention to the key factors shaping the economic landscape. At the heart of these developments are three powerful forces

- Monetary Policy: The tone is primarily set by the United States, with the Fed’s decisions influencing global financial markets.

- Industrial Policy: China is at the forefront, driving significant shifts in its economic structure towards sustainable and innovative industries

- Structural Policy: Europe continues to lead in setting the agenda for long-term structural changes and fiscal policies.

Global Market Outlook:

Navigating Volatility amid Fed Actions and Economic Slowdowns

The financial markets are gearing up for a volatile week as the much-anticipated Federal Reserve rate cut on September 18th looms closer. Historically, September has often been a challenging month for equities, and this year is proving no different. However, seasoned investors will remember that the final quarter of the year—October through December—has traditionally been favorable for stocks. With this in mind, the mantra “Buy the Dip” remains relevant, with a strong focus on asset allocation and global diversification as key strategies for capturing potential gains.

Global Economic Growth Concerns: The Slowdown in China and Germany

Adding to the market’s uncertainty are mounting concerns over the slowing economies of China and Germany. In Germany, the announcement that a leading car manufacturer is considering closing factories has become a powerful symbol of the challenges facing the nation. The aftermath of the Russia-Ukraine war has only exacerbated these issues, particularly for Europe, which once benefited from cheap Russian oil. The imposition of sanctions against Russia left Europe grappling with high energy costs, leading to a significant decline in industrial production—down 21% from pre-COVID levels and 17% from the peak of 2017.

China’s situation is more complex. As a relatively closed economy, China’s recent government policies have been supportive of boosting consumption and improving domestic sentiment. The country is gradually shifting away from its traditional reliance on real estate and property markets, pivoting towards new growth avenues such as electric vehicles (EVs) and their related ecosystems, green technology, renewables, tourism, and luxury goods. Rural consumption in China has remained resilient, largely insulated from the property crisis, while high-net-worth individuals (HNWIs) have redirected their spending to tourism, particularly in Japan, where a weaker yen is impacting luxury sales. This has positioned China in a unique “sweet spot”—a market worth considering when others are hesitant.

Market Dynamics: Fed Actions, Yen Carry Trade, and Tech Sector Risks

The upcoming Fed rate decision is not the only factor weighing on the markets. A third concern is the disorderly unwinding of the Yen carry trade, which has been complicated by the Bank of Japan’s (BOJ) recent statements signalling further rate hikes in Japan this year. This has yet to fully play out, particularly in the technology sector, which has benefited significantly from riskier asset inflows fueled by a weaker yen.

Another issue is the market structure itself. The “Magnificent Seven” rally in the U.S. has stalled, contributing to heightened volatility in a market already showing signs of concentration. The U.S. CAPE (Cyclically Adjusted Price-to-Earnings) ratio is currently trading above historical standards, raising concerns that the U.S.’s dominant weight in global indices, based on earnings growth and market capitalization, may soon face a rebalancing.

Weekly Market Snapshot: Key Events and Outlook

- Monday

China: CPI expected at 0.7% MoM, providing insight into inflation trends.

- Wednesday

US: CPI projected to fall to 2.6%, signaling potential for a 50bps Fed rate cut.

UK: GDP data could support further BoE rate cuts if it exceeds expectations.

- Thursday

EU: ECB likely to cut rates by 25bps, with focus on Lagarde’s guidance for future cuts.

US: PPI expected to rise 0.2%, which may challenge expectations of a significant rate cut. Jobless Claims remain crucial post-NFP report.

- Friday

US: Michigan Consumer Sentiment forecasted to rise to 68, impacting equity markets.

EU: Industrial Production expected to rebound 0.2%, supporting further ECB rate cuts.

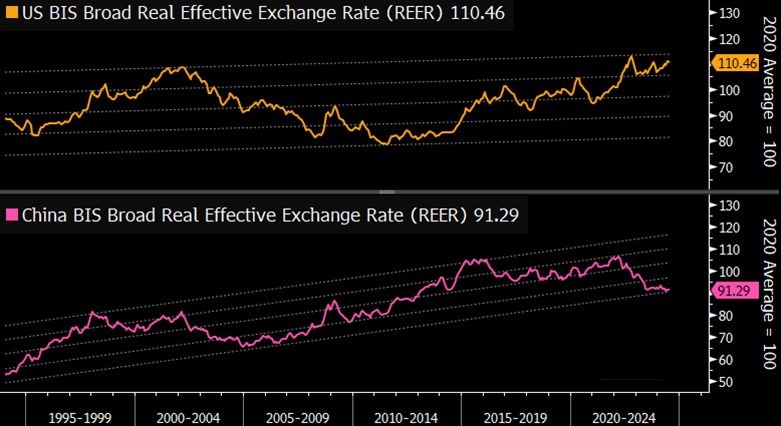

The U.S. Dollar and Trump’s Trade Strategy

Recent comments by Donald Trump suggest he might impose a 100% tariff on countries that stop using the U.S. dollar, aiming to protect American manufacturing. Trump argues that a strong dollar makes U.S. goods more expensive and less competitive, while weaker currencies like the Japanese yen and Chinese yuan give those countries a trade advantage. However, imposing tariffs on countries with weaker currencies could backfire, as they might further devalue their currencies to offset the impact, escalating trade tensions.

The Real Effective Exchange Rate (REER) highlights this dynamic:

- U.S.: The REER has been rising since 2011, nearing its 2022 peak, which strengthens the dollar but harms U.S. trade competitiveness.

- China: The REER has dropped since 2022, making Chinese goods cheaper and more competitive globally.

Key Points of Discussion:

- Dollar Centrality: The U.S. dollar remains central to global trade, finance, and reserves

- Contradictory Beliefs: Opinions differ on whether this centrality is a burden or a strategic necessity for the U.S

- Economic vs. Diplomatic Views: Economically, the dollar’s central role may be overstated, but diplomatically, the U.S. views maintaining dollar dominance as crucial for its global influence.

In summary, while the economic arguments around the dollar’s centrality may be debated, the U.S. sees it as vital for maintaining its global diplomatic power.

Bond Market Update

The global bond rally has gained momentum, driven by muted Chinese performance, economic concerns in the U.S. and weak economic figures in the Eurozone. The value of global bonds rose reaching $69.29 trillion, close to an all-time high despite the high interest rate environment.

The fact is M2 supply had receded a bit, which will bring down the inflationary concern, but the investment flows is Fixed asset instrument’s highlight’s that inflation story is here to stay.

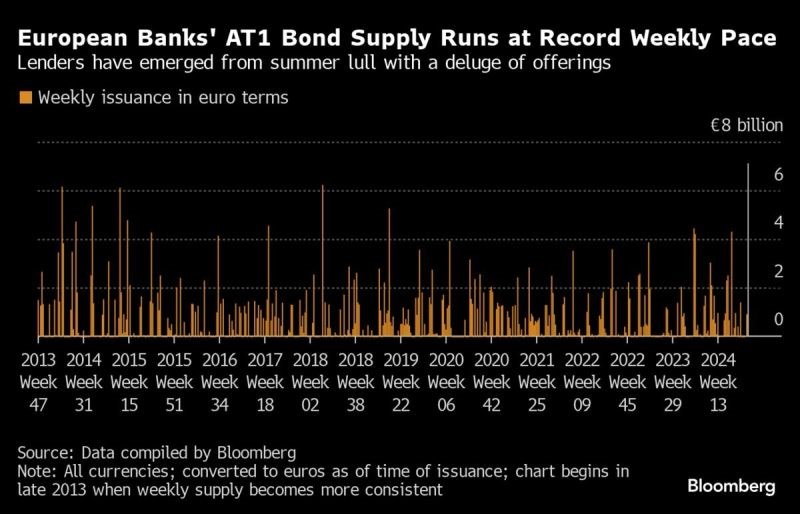

AT1 Bond Sales Surge Amid Central Bank Rate Cut Expectations

This week saw a record issuance of Additional Tier 1 (AT1) bonds, a type of risky bank debt introduced post-global financial crisis. European banks, which dominate the AT1 market, raised €7.1 billion ($7.9 billion), setting a new weekly record. Major institutions like UBS, HSBC, and BNP Paribas contributed to this surge as investors rushed to lock in yields, anticipating the Federal Reserve’s potential rate cuts.

Yields on AT1 bonds are now near their lowest in over two years, driven by a significant reduction in credit spreads following the Credit Suisse debacle and declining yields ahead of expected central bank rate cuts.

Asian Markets

The Asia-Pacific region saw mixed performances (Last week), with most markets ending the week on a down note. Tokyo marked its fourth consecutive session of losses, falling by 0.7%. Mainland China dipped 0.3%. Other major markets like India (-0.9%) and South Korea (-1.3%) also declined. However, Australia (+0.3%) and Taiwan (+1.1%) managed to post gains on the final day, although they couldn’t offset their overall weekly losses.

Meanwhile, European markets opened slightly in the red, reflecting ongoing investor nervousness ahead of the U.S. jobs report published which was tepid and below forecast.

Indian Market Update

India’s stock market rally is creating a dilemma for global fund managers. Despite India’s promising growth outlook, with the economy expected to grow at over 7% for the next decade, concerns over high valuations are leading some managers to hold back on increasing their allocations mirroring India’s weight in global broader indices. This hesitation puts them at risk of underperforming relative to their benchmarks.

India’s strong economic prospects are driven by a shift from a service-dominated economy to one focused on manufacturing, which creates five times more jobs than services. Government policy, increased pvt capex, and private sector investment are expected to support this growth, along with rising consumption. If mid-teen earnings growth continues, it would justify current valuations and boost investor confidence, ensuring that capital flows continue, there by seems expensive then will be fairly conservative.

Despite Foreign Institutional Investors (FII) selling over Rs 5.5 lakh crores from January 2022 to August 2024, robust domestic inflows exceeding Rs 11 lakh crores have consistently supported the market, with every dip being met with strong buying.

Disclaimer: This article provides general information existing at the time of preparation and we take no responsibility to update it with the subsequent changes in the law. The article is intended as a news update and Affluence Advisory neither assumes nor accepts any responsibility for any loss arising to any person acting or refraining from acting as a result of any material contained in this article. It is recommended that professional advice be taken based on specific facts and circumstances. This article does not substitute the need to refer to the original pronouncement

CLICK HERE DOWNLOAD PDF