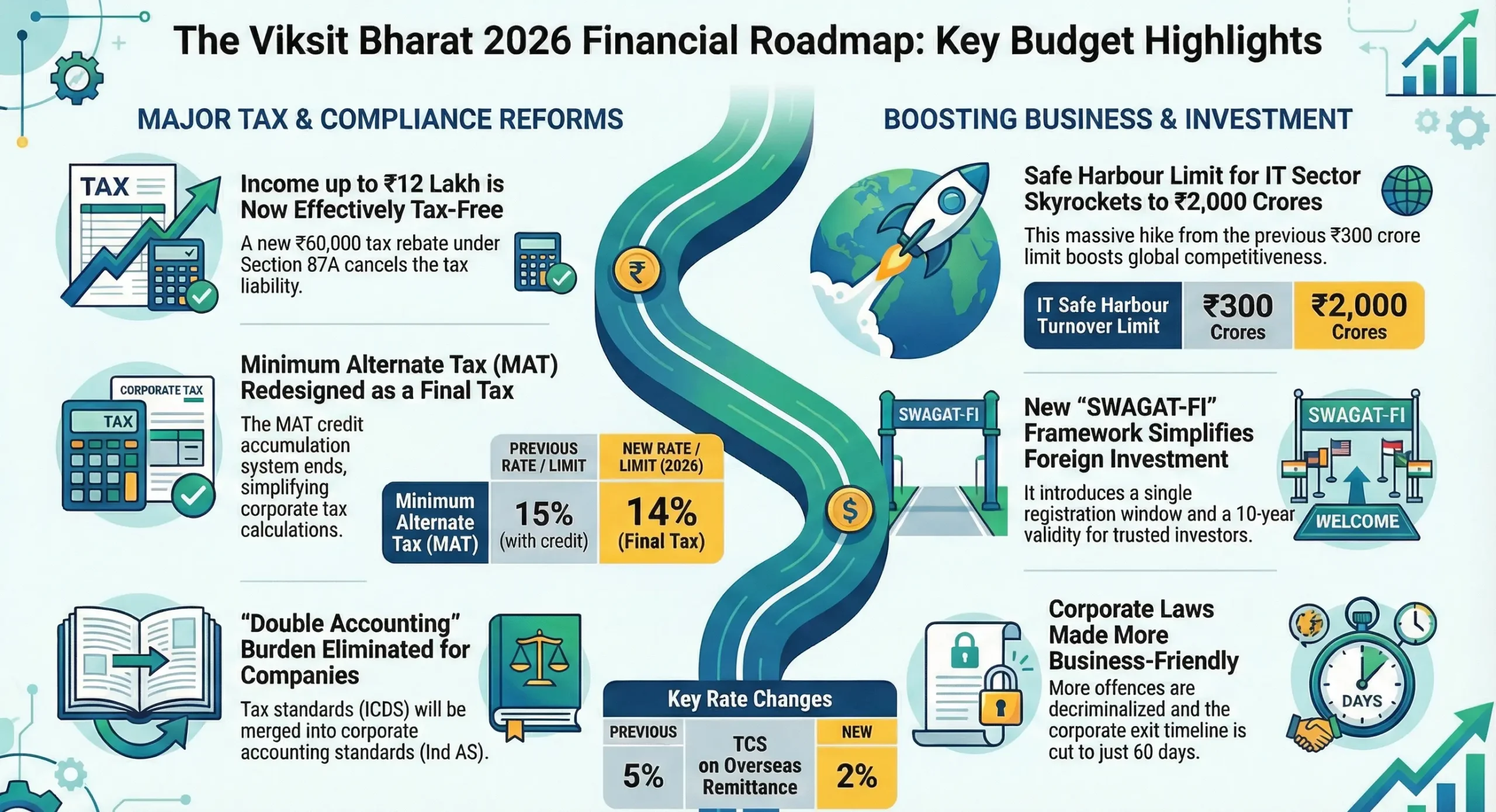

The Union Budget 2026-27, presented today by Finance Minister Nirmala Sitharaman, is a strategic pivot toward structural modernisation and fiscal discipline. With a total expenditure pegged at ₹53.5 lakh crore, the budget doubles down on long-term growth through a capital expenditure outlay of ₹12.2 lakh crore (a ~9% increase).

The centrepiece of this budget is the “Trust-Based Compliance” model, headlined by the rollout of the New Income Tax Act, 2025. By narrowing the fiscal deficit target to 4.3% of GDP, the government has sent a clear signal of stability to global markets while aggressively funding “frontier sectors” like semiconductors and biopharma.

- Personal Taxation: The 2025 Act & The “Zero-Tax” ₹12 Lakh Threshold

The most significant change for individuals is the full implementation of the New Income Tax Act, 2025, which aims to replace the legacy 1961 code with a lean, digital-native framework.

- No Slab Change, High Rebate: While the basic slab rates remain the same as last year, the Section 87A rebate has been increased to ₹60,000. This makes income up to ₹12 lakh effectively tax-free under the New Tax Regime.

- Standard Deduction: Maintained at ₹75,000 for salaried employees.

- Staggered Filing Deadlines: To reduce portal crashes, ITR-1 and ITR-2 (individuals) are due by July 31, while non-audit businesses have until August 31.

- Revised Returns: The window for filing a revised return has been extended to March 31 (with a nominal fee).

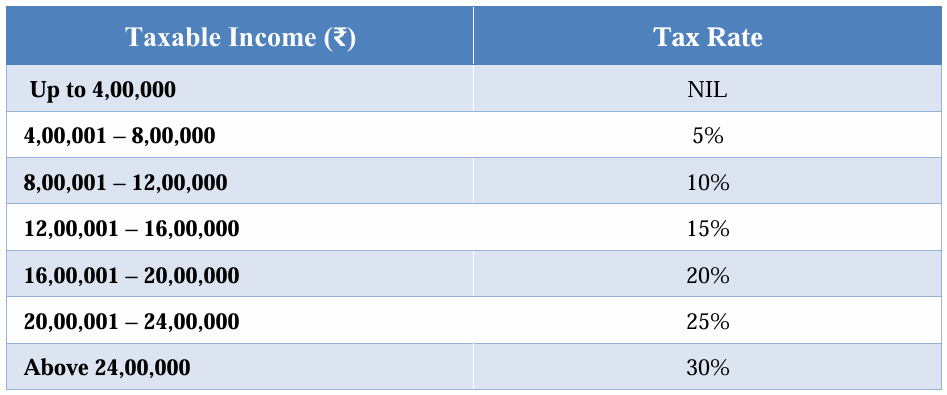

The Math: How an Income of ₹12 Lakh Becomes Tax-Free

Under the New Tax Regime, tax is calculated on slabs, but the Section 87A rebate cancels out the liability for resident individuals.

- Step 1: Calculate Tax on Slabs

- ₹0 – ₹4,00,000: Nil

- ₹4,00,001 – ₹8,00,000: ₹20,000 (5% of ₹4 lakh)

- ₹8,00,001 – ₹12,00,000: ₹40,000 (10% of ₹4 lakh)

- Total Tax Calculated: ₹60,000

- Step 2: Apply the Section 87A Rebate

- The 2026 Budget provides a rebate of up to ₹60,000 for incomes up to ₹12 lakh.

- Final Tax Payable: ₹60,000 (Tax) – ₹60,000 (Rebate) = ₹0.

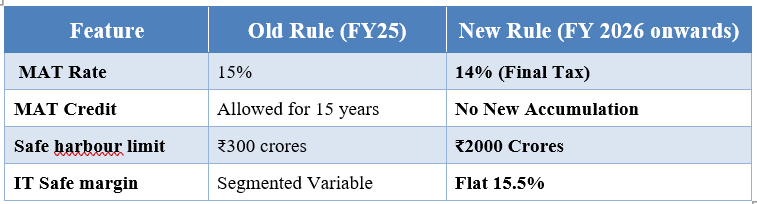

MAT Reforms: From Credit Mechanism to Final Tax

The government has fundamentally redesigned MAT to simplify the tax code and push companies toward the New Corporate Tax Regime (concessional 22% rate).

- MAT as Final Tax: From April 1, 2026, MAT is proposed to be a terminal levy. This means companies will no longer accumulate “MAT Credit” to offset against future regular tax liabilities.

- Rate Reduction: To compensate for the loss of the credit mechanism, the MAT rate is reduced from 15% to 14% of book profits.

- Encouraging the New Regime:

- Restriction on Old Regime: Companies staying in the old tax regime will not be allowed to set off their existing brought-forward MAT credit.

- Incentive for New Regime: Companies that shift to the New Tax Regime can utilise their accumulated MAT credit, but it is capped at one-fourth (25%) of the total tax liability in a given year.

- Non-Resident Exemption: Foreign companies and non-residents paying tax on a presumptive basis are now entirely exempt from the MAT framework.

Accounting Standards: Harmonising ICDS and Ind AS

In a massive move to reduce the “Double Accounting” burden, the government is merging tax-based standards with corporate accounting standards.

- Integration of ICDS: A joint committee comprising the Ministry of Corporate Affairs (MCA) and the CBDT has been formed to incorporate the requirements of Income Computation and Disclosure Standards (ICDS) directly into the Indian Accounting Standards (Ind AS).

- Discontinuation of Dual Reporting: The separate accounting framework for tax purposes (ICDS) will be done away with starting from the tax year 2027-28.

- Single Set of Books: This move ensures that companies won’t have to maintain two different sets of profit calculations for corporate law and tax law, drastically cutting down on compliance costs and litigation.

Safe Harbour Rules: Scaling for Global Competitiveness

The budget has aggressively expanded the “Safe Harbour” regime to position India as a global hub for services and Global Capability Centres (GCCs).

- Massive Threshold Hike: The turnover threshold for the IT sector to avail of Safe Harbour benefits has been hiked from ₹300 crores to ₹2,000 crores.

- Unified Category: Multiple segments like Software Development, ITeS, KPO, and Contract R&D are now clubbed under a single “Information Technology Services” category.

- Fixed Margin: A uniform Safe Harbour margin of 15.5% will apply across this unified category.

- Automated Approval: To eliminate “taxman interference,” safe harbour applications will now be approved through an automated, rule-driven process without requiring manual scrutiny by tax officers.

Impact Summary: MAT vs. Safe Harbour

* Critical Note for Salaried Employees: With the ₹75,000 Standard Deduction, the effective zero-tax threshold for salaried individuals is actually ₹12.75 lakh. If your gross salary is ₹12.75 lakh, your taxable income becomes ₹12 lakh after deduction, making your tax Nil.

- NBFC Evolution: Building the “Credit Frontline” for MSMEs

The budget transitions NBFCs from “shadow banks” to the primary delivery arm for India’s credit growth, particularly for the MSME and “Sunrise” sectors.

- PFC-REC Restructuring: The government is restructuring Power Finance Corporation (PFC) and Rural Electrification Corporation (REC) to create massive, sovereign-backed NBFCs capable of funding India’s green energy transition.

- SARFAESI Reform: The threshold for NBFCs to invoke the SARFAESI Act for debt recovery is being reviewed for a reduction to ₹1 lakh (from ₹20 lakh), providing them parity with banks for small-ticket lending.

- High-Level Committee on Banking: A new panel will review the entire banking and NBFC ecosystem to align it with the “Viksit Bharat” vision, focusing on technology adoption and risk management.

- SME Growth Fund: Channelled through NBFCs, a ₹10,000 crore fund will provide equity and growth capital to high-potential small enterprises.

- RBI & FEMA: “SWAGAT” to Global Capital

The RBI and Finance Ministry have introduced the SWAGAT-FI Framework to simplify how global money enters India.

- Single Window Registration: The “Single Window Automatic and Generalised Access for Trusted Foreign Investors” (SWAGAT-FI) consolidates FPI and FVCI regimes.

- 10-Year Validity: Registration and KYC validity for trusted foreign investors have been extended from 3 years to 10 years, drastically reducing compliance friction.

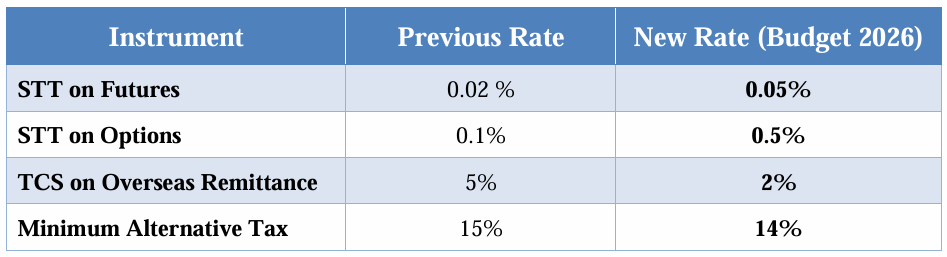

- TCS Rationalisation (LRS): TCS on remittances for education and medical purposes has been slashed from 5% to 2%, providing significant relief for families with overseas expenses.

- Foreign Asset Immunity: A “Small Asset” immunity window allows taxpayers to declare non-immovable foreign assets below ₹20 lakh without fear of prosecution, targeting “unintentional” non-compliance.

- Companies Act: Decriminalisation & The “Corporate Mitra”

The Ministry of Corporate Affairs (MCA) is shifting toward a supportive “facilitator” role for Indian businesses.

- Decriminalisation Phase 3: A further 25 minor technical lapses under the Companies Act have been converted from criminal offences to civil defaults.

- Corporate Mitras: The government will develop a cadre of ‘Corporate Mitras’ in Tier-II and Tier-III towns. These professionals will act as affordable compliance mentors for local MSMEs.

- C-PACE Expansion: The voluntary corporate exit timeline has been reduced from 180 days to 60 days, allowing for a faster “fail-and-restart” cycle for entrepreneurs.

- AIF, PE, VC, & Mutual Funds: Incentivising Long-Term Equity

The budget aims to curb speculative “churn” in the markets while rewarding stable, productive investments.

- STT Hike (F&O): To discourage excessive retail speculation, the Securities Transaction Tax (STT) on Futures is now 0.05%, and Options is 0.15%.

- Buyback as Capital Gains: Share buybacks will now be treated as Capital Gains in the hands of the shareholder (allowing for cost offset), rather than a deemed dividend.

- AIF Pass-Through Clarity: Category I & II AIFs have received further tax certainty, ensuring their investments are classified as “Capital Assets” rather than business income, preventing double taxation.

- Mutual Fund Interest Deduction: Taxpayers can no longer deduct interest costs incurred to earn dividend or MF income, simplifying the tax calculation but removing a minor arbitrage opportunity.

Closing Note: Scaling the $7 Trillion

VisionThe Union Budget 2026-27 signals a pivot from recovery to “Transformation and Scale.” By anchoring a ₹12.2 lakh crore Capex (9% hike) alongside a disciplined 4.3% fiscal deficit, India reinforces its standing as a stable, high-growth global engine.

Market Dynamics & Outlook

Despite a “wait-and-watch” correction fuelled by the STT hike on F&O and a 6% crash in bullion prices, the outlook remains bullish. The STT hike is a strategic “cooling mechanism,” designed to transition retail energy from speculative day-trading toward sustainable, delivery-based wealth creation.

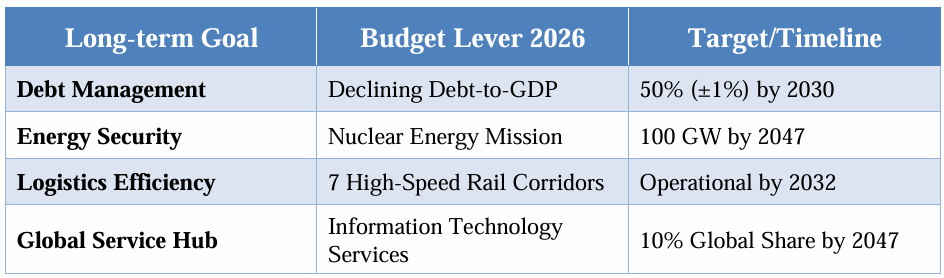

The “Viksit Bharat” Dashboard (2026-27)

- Proposed Amendment under GST in Union Budget 2026

1. Amendment in Post-Supply Discount – Section 15(3)(b) of CGST Act, 2017

Section 15(3)(b) is proposed to be amended to remove the requirement of linking post-supply discounts with a pre-existing agreement. The amendment also mandates reference to credit note issuance under Section 34, subject to reversal of proportionate ITC by the recipient.

Impact:

- Post-sale discounts will no longer be directly reduced from the taxable value.

- Mandatory issuance of credit note under Section 34.

- Recipient must reverse corresponding ITC linked to the discount.

- Alignment between valuation and credit note mechanism.

2. Amendment in Credit Note Provisions – Section 34 of CGST Act, 2017

Section 34 is proposed to be amended by inserting the words:

“or where a discount referred to in clause (b) of sub-section (3) of section 15 is given”

after the words “both supplied are found to be deficient”.

Impact:

- Explicit statutory backing for issuing credit notes for post-supply discounts.

- Legal linkage created between Section 15 valuation provisions and Section 34 credit note provisions.

3. Amendment in Refund Processing – Section 54(6) of CGST Act, 2017

In sub-section (6) of Section 54, after the words “supply of goods or services or both”, the following is proposed to be inserted:

“or of unutilised input tax credit allowed under clause (ii) of the first proviso to sub-section (3)”

Impact:

- Provisional refund mechanism will now also cover eligible unutilised ITC refunds.

- Faster processing and improved liquidity for eligible taxpayers.

4. Amendment in Refund Restriction Clause – Section 54(14) of CGST Act, 2017

In sub-section (14), after the words “sub-section (5) or sub-section (6)”, the following words are proposed to be inserted:

“, other than cases where refund of tax is claimed on account of goods exported out of India with payment of tax,”

Additionally, Section 54(14) is being amended to remove the minimum refund sanction threshold of Rs. 1,000 in cases of export of goods with payment of tax.

Impact:

- Refund restriction threshold of Rs. 1,000 will not apply to export refunds with tax payment.

- Small exporters will be able to claim refunds without monetary limitation.

- Improved cash flow and ease of compliance for exporters.

5. Amendment in Appellate Authority Framework – Section 101A of CGST Act, 2017

A new sub-section (1A) is proposed to be inserted which provides that:

Pending constitution of the National Appellate Authority, the Central Government may, on GST Council recommendations, empower any existing Tribunal to hear appeals under Section 101B.

It is also proposed that sub-sections (2) to (13) of Section 101A shall not apply where such Tribunal is empowered.

Effective Date: 1st April 2026

Impact:

- Interim dispute resolution mechanism enabled.

- Reduced backlog of Advance Ruling appeals.

- Faster adjudication process.

6. Amendment in Place of Supply – Intermediary Services (Section 13(8)(b) of IGST Act, 2017)

Clause (b) of sub-section (8) of Section 13 is proposed to be omitted.

As a result, the place of supply for intermediary services will be governed by the default rule under Section 13(2), i.e., location of the recipient of services.

Impact:

- Intermediary services provided to foreign clients may qualify as export of services.

- Reduced tax burden on cross-border service providers.

- Alignment with international GST/VAT principles.

- Major litigation relief for service exporters.

- Overall Compliance Takeaways

- Businesses must rework discount policies and credit note workflows.

- Exporters and refund claimants will benefit from procedural relaxations.

- Intermediary service providers should reassess place of supply and taxability structure.

- Advance ruling appeal mechanism gets interim institutional support.

- These amendments are proposed changes under Union Budget 2026 and shall become effective upon enactment and notification.

- For impact assessment, implementation planning, or compliance restructuring, our GST team remains available.

- Budget is pushing the importance of Gift City by making good alternatives for investment for FIIs

You are an FII/Hedge Fund looking to trade Indian Markets (especially Derivatives), here is why the GIFT City Route is mathematically superior to the traditional Mauritius/Singapore route.

1. Tax on Derivatives (F&O)

Mumbai (NSE/BSE): 30% Tax. Most FIIs are taxed at 30% (or 40%) on speculative business income if they trade derivatives, unless they have specific treaty protection.

GIFT City: 0% Tax. Capital gains on derivatives traded on the IFSC exchange are 100% Tax Exempt.

2. Transaction Taxes (The Cost of Trading)

Mumbai (NSE/BSE): High Impact. You pay STT (Securities Transaction Tax) on every trade. The Budget 2026 just hiked STT on F&O significantly.

GIFT City: Zero. No STT, no CTT, no Stamp Duty. Your high-frequency strategies work better here because friction costs are near zero.

3. Currency Operations (The Conversion Benefit)

Mumbai: Conversion Cost. You must convert USD to INR to trade. You pay conversion spreads (0.5% – 1%) and face depreciation risk on your idle cash balance.

GIFT City: Dollar Settlement. You trade and settle in USD. You save the 1% conversion cost on entry/exit. Your capital (cash) remains in hard currency, eliminating currency risk on your undeployed funds.

4. Fund Management Tax (The GP’s Profit)

Mumbai: Taxable. The Fund Manager’s management fee is taxed at standard corporate rates (25%+).

GIFT City: 100% Tax Holiday. The Fund Management Entity (FME) gets a 100% Corporate Tax Exemption for 10 years.

5. Relocation (Moving the Fund)

Mumbai: Tax Event. Moving assets from a Mauritius fund to an India fund is usually treated as a “Transfer” (Taxable).

GIFT City: Tax Neutral. The Budget allows “Grandfathering.” If you relocate your offshore fund to GIFT City, the transfer is Tax-Free for both the Fund and the Investors.

Final Perspective

This budget is not characterised by “big-bang” populist giveaways but by the unseen plumbing of a developed nation: a more modern Income Tax Act, a more professionalised NBFC sector, and a trust-based corporate environment. For professionals, the message is clear: Formalise, Digitalise, and Scale. The era of navigating complex legacy laws is being replaced by a “Plug-and-Play” India.

“The numbers in this budget are a reflection of our Kartavya (duty) to build a resilient, competitive, and innovative India.” – Nirmala Sitharaman, Union Budget Speech, 2026.

Disclaimer: This article provides general information existing at the time of preparation and we take no responsibility to update it with the subsequent changes in the law. The article is intended as a news update and Affluence Advisory neither assumes nor accepts any responsibility for any loss arising to any person acting or refraining from acting as a result of any material contained in this article. It is recommended that professional advice be taken based on specific facts and circumstances. This article does not substitute the need to refer to the original pronouncement.

CLICK HERE DOWNLOAD PDF